Stopped Process is also R.C. Martingale

Theorem (Stopped Process is also right-continuous Martingale)

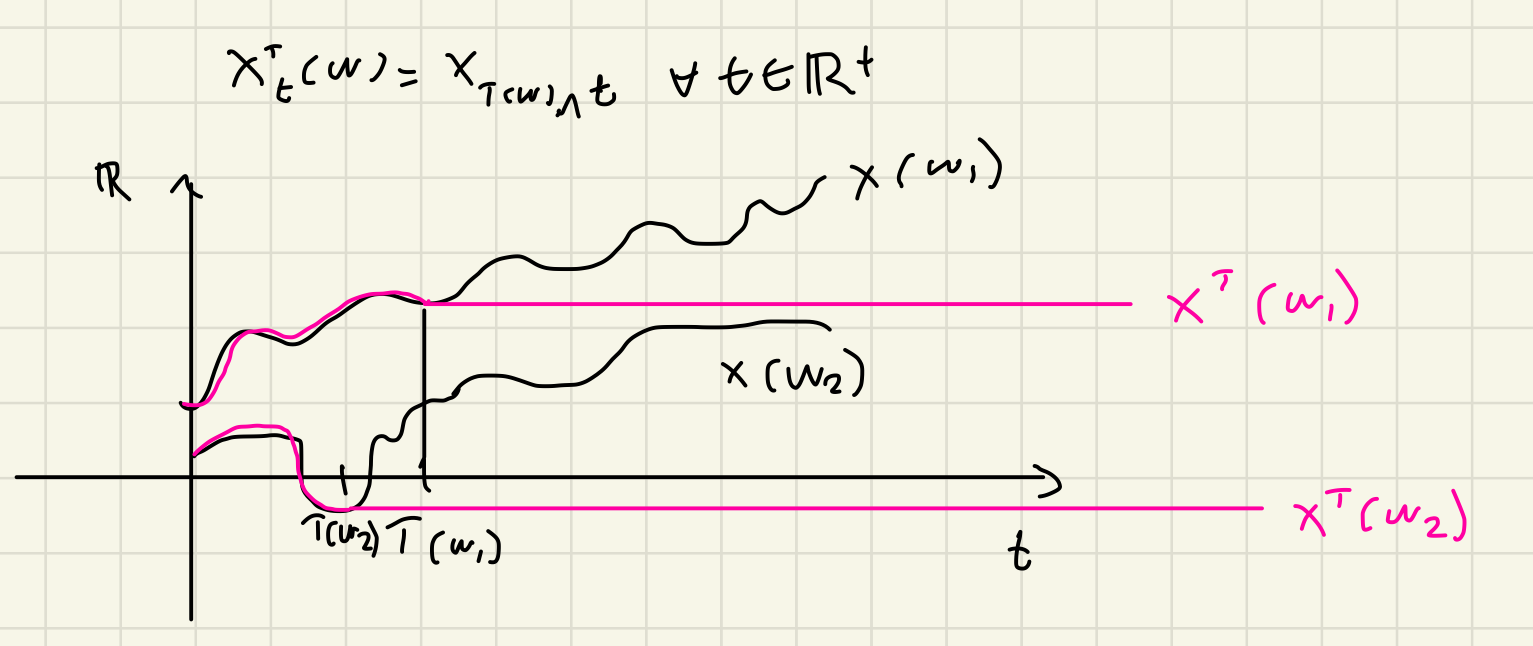

Let be a right continuous -martingale and let be a -stopping time. Then is a right continuous -martingale.

Theorem (Stopped Process is also right-continuous Martingale)

Let be a right continuous -martingale and let be a -stopping time. Then is a right continuous -martingale.